Microsoft word - scf_new dimension to b2b trade_poms_conf.doc

Dynamic Payables Discounting: A Supply Chain Finance Perspective Preetam Basu

Department of Operations and Information Management

Suresh Nair

Department of Operations and Information Management

Dynamic Payables Discounting: A Supply Chain Finance Perspective

Supply Chain Finance (SCF) is emerging as the next frontier in Global Supply

Chain Management that firms are focusing on to drive financial advantage over

their competitors. A wide variety of innovative trade solutions are currently being

developed by merging physical supply chain information with financial supply

chain data. Based on event triggers, SCF providers are offering much needed

liquidity at different points of the supply chains. These SCF products are

transforming traditional working capital management. In this paper we study the

payables management problem of a buying firm in a supply chain scenario with

SCF enabled “Early Payment Program” implemented. In this paper we develop a

stochastic dynamic programming model to capture the uncertainties and the

temporal aspects of short-term cash management.

(Global Supply Chain Management, Supply Chain Finance, Working Capital Management, Stochastic Dynamic Programming) 1 Introduction

The focus of Supply Chain Management (SCM) to date has been streamlining and automating

the physical supply chain in order to reduce costs. Significant improvements have been

achieved in physical supply chain management over the last few decades. However as physical

supply chains have become more and more optimized, savings have become harder to realize.

This has prompted supply chain managers to focus their attention on other aspects of the

supply chain in order to achieve further gains.

One aspect of the supply chain that has been largely overlooked is the financial side of

SCM. Managers till now have not been able to fully leverage the earning potential of business-

to-business (B2B) trade. For every physical order working its way up the supply chain, a

financial transaction moves in the other direction. Firms today compete on a global platform. To

achieve cost benefits, retailers often source materials from suppliers in countries with lower

labor and raw materials costs like China, India or Vietnam. This production outsourcing has

helped retailers achieve significant reduction in their operating costs. But when it comes to their

treasury operations, the buyer and the supplier perform roles that are in conflict. Due to this lack

of collaboration in treasury management, supply chains fail to achieve potentially large financial

In a typical supply chain scenario the buyer’s primary motivation is to stretch payables

and earn interest off the float. This tendency of the buyer improves its working capital position

but adversely affects the cash flows of its suppliers. Global suppliers, who are mostly in the

emerging markets, have constricted access to short term financing and a much higher cost of

capital. To meet their business needs such suppliers have to arrange for financing at exorbitant

rates. Cost shifting to suppliers result in better Days Payables Outstanding (DPO, a metric that

indicates how many days on average an organization takes to settle its payables) for the buyers

but leads to a financially unstable supply base and to higher costs of the products.

In the last few years supply chain service providers and financial institutions have come

up with many solutions to release trapped value in B2B trade. This has led to the emerging field

of Supply Chain Finance (SCF). SCF can be defined as a combination of technology and trade

financing that unites the buyer, the supplier and a financial intermediary electronically to provide

financing triggers based on one or more supply chain events. Using these services, buyers can

not only extend their DPOs but also leverage their higher credit ratings to provide better

financing for their suppliers and as a result improve the overall performance of the supply chain.

The main focus of these solutions is to provide supply chain partners with more control over

their financial processes and more options on how to optimally use cash and credit. Financing

is made possible at different points of the supply chain based on event triggers like purchase-

order issuance, invoice issuance, advanced shipping notices and invoice approval.

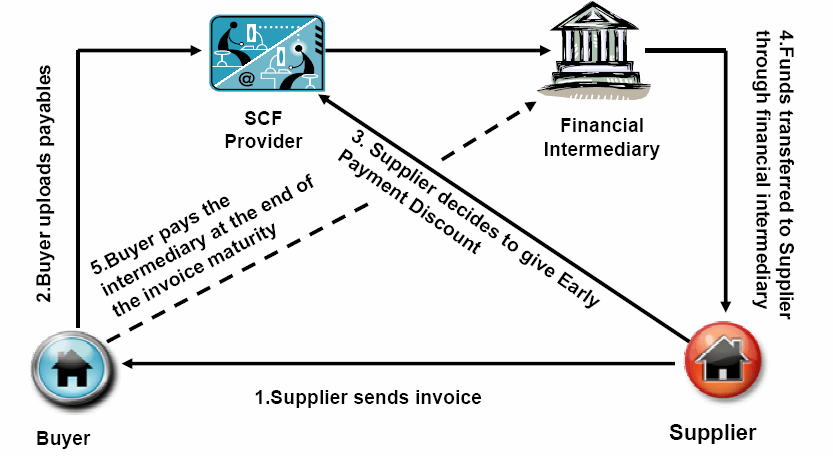

In this paper we focus on one of the key aspects of SCF, the Early Payment Discount Program from the standpoint of payables management for the buyer (see Figure 1).

Figure 1: Early Payment Discount Program Early Payment Discount Program

Businesses typically focus on getting paid as quickly as possible reducing their days sales

outstanding (DSO) and delaying paying suppliers for a long as possible by extending days

payables outstanding (DPO). This leads to an obvious conflict of interest between the buyers

and their suppliers based on working capital management objectives.

In order to reduce their DSO, which is an important measure of an organization’s

operational efficiency on their sales side, and to obtain cash early, supplier’s offer early payment

discounts to its buyers. One of the most common trade terms used by the suppliers is “2/10, Net

30”. This allows the buyer to take a two percent discount on the face value of the invoice if they

pay within ten days. Otherwise, they must pay the full amount within thirty days. Since global

suppliers need access to capital which is limited and expensive, it is worthwhile for them to give

discounts on their invoices and be paid faster rather than obtaining loans using their own credit

Taking advantage of a 2% discount to pay 20 days early amounts to a buyer realizing an

annualized return of almost 36%. This high rate of return far outweighs almost any other short

term investments the buyer may consider. So it’s imperative for the buyer to take the early

payment discounts rather than extend payables. But for a typical buyer this cash earning

opportunity goes unrealized as they may not have the technology in place to take advantage of

the early payment discounts. Lack of visibility in the payables management system leaves too

many early payment discounts out of reach of the buyer.

SCF providers now offer buyers automated services to better manage their accounts

payables and in turn optimize their working capital. This is a win-win for both buyer and seller, it

helps the buyer extend their DPOs and at the same time provides fast access to capital for the

suppliers. This is the way it works – the supplier sends the goods to the buyer along with the

invoice and checks the intermediaries B2B site for material acceptance and the clearing of the

invoice, when a material is accepted by the buyer the SCF site is informed and if the supplier

decides to give a discount the financial intermediary is directed to pay off the invoice (less

discount) to the supplier in the specified time (10 days with discount), the supplier is

immediately informed by the intermediary and the payment made. The whole process is now

continuously visible by all parties. On the regular maturity of the invoice the buyer pays off the

financial intermediary. The early payment discount gets shared between the intermediary and

the buyer and the seller obtains the cash early which in turn serves his purpose. The

intermediary provides the cash based on the credit rating of the buyer as the credit is secured

against the accounts payable of the buyer. In this setup the buyer can avail third party credit to

capture the early payment discounts and at the same time extend the payable to the maturity

date of the invoice, the suppliers can get cash early and improve their trade cycle and the

financial intermediary can inject capital at a lower risk (Figure 1).

In this paper we analyze payables management of a buyer who has an early payment

program implemented through SCF. A two percent discount on the face value of an invoice may

not sound too exciting but for larger buyers who have billions tied up in payables this may result

in savings of millions of dollars. As we have seen above, capturing the early payment discounts

is extremely imperative from the buyer’s perspective. But even the strongest buyer does not

always have cash sitting around to take the early payment discounts when the need arises and

in many circumstances are forced to extend payables. Hence it’s essential for the treasury

manager of the buying firm to develop a payable mechanism that combines the use of its own

cash reserves and SCF provided financing to create a cost-advantaged supply chain. In this

paper we develop optimal decision rules for the accounts payable management of the buyer

Working Capital Management and SCF

Corporate finance, on a broad level, can be classified based on long-term and short-term

decisions and techniques. Capital investment decisions like which projects receive investment,

whether to finance that investment with equity or debt, merger and acquisitions policies or

whether and when to pay dividends to shareholders are termed as long-term financial decisions.

On the other hand, cash flows connected with the day-to-day operations of the firm are grouped

under short-term financial management. Short-term financial management encompasses

decisions about activities that affect cash inflows, cash outflows, backup liquidity like bank credit

line or loan management and internal cash flows. These short term financial decisions are

grouped under the heading "Working Capital Management"(WCM).

Efficient WCM is vital towards functioning of any corporation. It directly impacts the

operating cash flows of the firm. Incorrect evaluation of a firm’s working capital requirements

may cause severe losses and adversely affect its long-run prospects. Similarly proficient short

term financial decisions can generate significant improvement to a firm’s return on investment

and improve share holder’s value. Because of its importance to the survival of firms, WCM

occupies major portion of a treasury manager’s time. Lack of synchronization between cash

inflows and outflows and the intrinsic difficulty in forecasting these quantities on a day-to-day

basis make WCM really complex and challenging. The key to competent WCM lies in adjusting

the firm’s asset and liability mix continuously to smoothen the stochastic variations in cash

flows. Here we look at the academic literature on short-term financial management.

WCM is multidimensional in nature and requires active involvement of the finance,

production and marketing departments. Hence researchers from various fields such as finance,

economics and operations management have studied the working capital and liquidity

management problem. The earliest work on cash management is by Baumol (1952). He

examined the cash-balance problem as an inventory management problem of some physical

commodity. The problem setting was deterministic where the net cash flow was known with

certainty. Miller and Orr (1966) also considered stochastic cash management problems. They

derived the control-limit policy parameters for optimal cash holdings. Eppen and Fama (1969,

1971) and Constantinides (1976) also developed analytical models to capture the uncertainty

and temporal aspect of the cash management problem. These models provide insight into the

qualitative structure of the optimal cash-balance policy and the transactions demand for cash.

Girgis (1968) and Neave (1970) formulated the cash management problem as a multi period

inventory problem. Extensive surveys of the development of this literature was provided by Elton

and Gruber (1975) and Ziemba and Vickson (1975).

Other prominent studies in the field of short-term financial management include work by

Maier and Van der Weide (1978) and Robichek et al. (1965). To capture the stochastic element

of the cash management problem researchers developed chance-constrained and linear

programming under uncertainty models (LPUU). Charnes and Thore (1966) and Pogue and

Bussard (1972) developed chance-constrained programming models of the cash management

problem. LPUU models developed by Kallberg et al (1982) provide another approach to treat

the uncertainty associated to cash management.

A Stochastic Dynamic Programming Model

We develop a finite horizon stochastic dynamic programming model to capture the uncertainty

and the inter-temporal aspect of the cash management problem. Here our focus is on the

payables management of the buying firm that has implemented an early payment program with

its suppliers. Early payment discount terms like “2/10 Net 30”, “3/20 Net 60” are quite common

in B2B trade. With SCF provided early payment solutions in place the treasurer has an

additional option to settle accounts payables (A/P). He can pay the invoices either with his firm’s

own cash reserves, or based on liquidity requirements, he can extend the payables and go for

SCF provided financing. Capturing the early payment discounts with own cash reserves is

always worthwhile as involving an intermediary requires profit sharing. But due to uncertainty in

future cash flows it is not obvious at each time period whether and by what amount should the

treasury use own cash reserves or go for SCF financing.

In our model we consider trade credit terms of the form “ r /10 Net 30” where r can be

any discount percentage e.g. 2%, 3%, etc. The discount period is taken as ten days and the

invoice maturity is thirty days. Other trade terms can be easily incorporated into the model. The

sum total of invoices arriving at any time period t is denoted by i . The accounts receivable (A/R)

and the cash on hand, i.e., the firm’s own cash reserves in any period are a and c

respectively. We interpret a as the net inflow of cash at any time period. Here a and c can

be positive or negative based on the cash flows and the payable decisions.

At the beginning of each time period t , the treasurer looks at the values of c , a , i and

decides what amount of i would be settled by own cash reserves and what would be funded by

SCF sources. Uncertainty in the payables management problem comes from future A/R and

respectively, which are stochastic and follow discrete probability distributions.

From period to period they are assumed to follow independent identically distributed probability

The actions in our model are the amounts of own cash reserves that the treasurer uses

at each time period. Then the amount of SCF provided cash used at any period would be the

difference of the invoice amount and the own cash used. For notational simplicity we call the

treasurer’s cash reserves “own cash” and SCF arranged credit “SCF cash” respectively. We

assume that at each time period payments are made in discrete units h , h , …, h from “own

cash” where 0 ≤ h < h < . < h ≤

Min c + a , i ] . The invoice amount that is paid through

own cash at t gets deducted from the cash reserves immediately. But the amount paid by SCF

cash affects the cash reserves after three time periods since the treasure has to repay the SCF

intermediary only at the maturity of the invoice.

denote the invoice amount that is funded through SCF sources at

t − 2 and t − 1 and that needs to be paid at t + 1 and t + 2 respectively. For analytical tractability

we have aggregated ten days as one time period. Let T be the time horizon for the problem.

Then the state of the system in a time period t can be specified by (c , a , i , zf (c , a , i , z

) be the maximal discounted net present value of being in state

(c , a , i , z

) when optimal actions are taken in each time period from period t to T . Firms

remain reluctant to use their credit capacity to fund early payment discounts as they require

bank loans and sound credit lines for other daily operations. In our model we assume that the

treasurer opts for bank loans only when he does not have adequate cash on hand to pay off an

invoice amount that had been stretched through SCF provided credit. In other words bank loan

is taken only to repay SCF credit. To ensure that the dynamic programming solution avoids

those states where bank loans are required we penalize them by a large rate of interest for the

Let r be the discount percentage that is earned by the buyer if the invoice is funded

through the SCF solution (r > r ) . We assume that after the payable decision has been made

the left-over cash is invested in a single period sweep account to keep the funds as liquid as

possible since the objective of the treasury is to avail as much of the discount with own cash.

Hence the cash invested at t matures at t + 1 and the treasury has that amount on hand before

he makes his decision at t + 1 . Let r be the rate of return on the one period sweep account

investment (r > r > r ) . Let β be the discount factor. Then the following recursive functional

f (c , a ,i , z

max P (c , a , i , h) + β[

E f T (c P (c , a , i , h) = r h + r (i − h) + r (c + a − h is the single period reward function;

E[ f T (c

∑∑ p(a )q(i ) f T (c − ,ha ,i ,z ,i − h f (c , a , i , zL(c + a ) + r i + β E[ T

The boundary condition for this model is:

f (c , a ,i , z

) = c + a − i − z

∀c , a , i , z4 Conclusions

Recent developments in the financial supply chains have made it imperative to analyze working

capital management in view of B2B trade financing. The innovative SCF products have started

to transform the traditional practices in short-term cash management. In B2B trade, early

payment discounts are often offered by suppliers in order to improve their cash flows. Most of

the times these discounts are out of reach of the buying organization because of lack of visibility

into the procure-to-pay cycle. With automated payables enabled by SCF providers, the buyer

now has an added opportunity to avail these early payment discounts. Through innovative

financing made possible by third party financers, buyers can simultaneously capture the early

payment discounts and extend the payables till the maturation of the invoice.

In this paper we develop a stochastic dynamic programming model to incorporate the

temporal and the uncertainties associated with short-term cash management and examine

payables management of a firm engaged in B2B trade. We are currently working on extensive

numerical analysis to gain critical managerial insights.

References

1. Baumol, W. J. 1952. “The Transactions Demand for Cash: An Inventory Theoretic

Approach,” Quarterly Journal of Economics, 66, pp 545-556.

2. Charnes, A., S. Thore. 1966. “Planning for Liquidity in Financial Institutions: The Chance

Constrained Method,” Journal of Finance, 21, pp 649-674.

3. Constantinides, G. M. 1976. “Stochastic Cash Management with Fixed and Proportional

Transaction Costs,” Management Science, 22(12), pp 1320-1331.

4. Elton, E., M. J. Gruber. Finance as a Dynamic Process. 1975. Prentice Hall, Englewood

5. Eppen, G. D., E. F. Fama.1969. “Cash Balance and Simple Dynamic Portfolio Problems

with Proportional Costs,” International Economic Review, 10(2), pp 119-133.

6. Eppen, G. D., E. F. Fama. 1971. “Three Asset Cash Balance and Dynamic Portfolio

Problems,” Management Science, 17(5), pp 311-319.

7. Girgis, N. M., 1968. “Optimal Cash Balance Level,” Management Science, 15, pp 130-

8. Kallberg, G., R. W. White and W. T. Ziemba. 1982. “Short-Term Financial Planning

under Uncertainty,” Management Science, 28(6), pp 670-682.

9. Maier, S. F., J. H. Van der Weide. 1978. “A Practical Approach to Short-Run Financial

Planning,” Financial Management, 7, pp 10-16.

10. Milller, M. H., D. Orr. 1966. “A Model of the Demand for Money by Firms,” Quarterly Journal of Economics, 80, pp 413-435.

11. Neave, E. H. 1970. “The stochastic cash-balance problem with fixed costs for increases

and decreases,” Management Science,16, pp 472–490.

12. Pogue, G. A., R. N. Bussard. 1972. “A Linear Programming Model for Short-Term

Financial Planning Under Uncertainty,” Sloan Management Review, 13, pp 69-98.

13. Puterman, M. L. 2005. Markov Decision Processes, Discrete Stochastic Dynamic

Programming, John Wiley and Sons, New York.

14. Robichek, A. A., D. Teichroew and J. M. Jones. 1965. “Optimal Short-term Financing

Decision,” Management Science, 12, pp 1-36.

15. Ziemba, W. T., R. G. Vickson. (eds) Stochastic Optimization Models in Finance, 1975,

How long does a hair transplant procedure take? It depends on the number of hair grafts that are transplanted and usual y ranges from 5 to 8 hours. Am I awake during the procedure?Yes. A local anesthetic is used to numb the scalp, al owing you to read, listen to music, watch television or sleep. Is a hair transplant painful?One of the main goals of the TrueHair™ program is to provide excel e

FOUNDATIONS OF INDIVIDUAL BEHAVIOR Finding and analyzing the variables that have an impact on employee productivity, absence, turnover, and satisfaction is often complicated. Many of the concepts—motivation, or power, politics or organizational culture—are hard to assess. Other factors are more easily definable and readily available—data that can be obtained from an employee’s person

Figure 1: Early Payment Discount Program

Figure 1: Early Payment Discount Program