Zen Daily Market Report - 04/09/2009 Particulars 03/09/2009 Gain+/Loss-

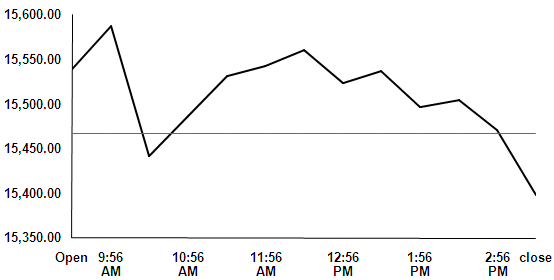

The Indian benchmark indices opened on a positive note but soon

witnessed volatility due to mixed cues from global markets and

fell under negative territory. However, they witnessed some buying

at lower levels and the markets regained the rally amid volatility.

They experienced a dull and sideways trade during the afternoon

session and the decrease in volumes was also been seen during the

day. But, on tracking the subdued opening of European markets

and profit booking by the investors the indices witnessed pressure

and closed in red. By the end of the trade, the BSE Sensex and

Nifty were marginally down by 0.45% and 0.32% to close at

15398.33 and 4593.55 respectively. There were 1402 advances and

1350 declines in BSE, indicating that there was selective buying in

Midcap and Smallcap space. At the sectoral level, Consumer Durables, Metals, IT and

Technology have performed well while Oil&Gas, Healthcare,

Capital Goods and Auto have witnessed pressure. 03/09/2009 Gain + / Loss -

Consumer Durables have performed well as Videocon and Titan

were up by 0.96% and 0.16% respectively. Metals space witnessed

interest as some of its majors have increased the steel prices. Tata

Steel, Hindustan Zinc, Sesa Goa, Welspun Gujarat and Sterilite

gained 1-1.64%. IT rallied as TCS, Infosys, Rolta and Mphasis rose

Oil&Gas space witnessed pressure since the diverting funds from

secondary markets to primary markets could be seen in view of

the coming IPO of Oil India. Cairn, Essar oil, RNRL, ONGC and

Reliance lost 0.43%-2.01%. Healthcare lost as Biocon, Dr Reddy’s,

Cipla and Ranbaxy fell by 0.56%-2.32%. Capital good was down

as Punj Lloyd, L&T, Siemens and BEML lost 1.03% to 2.7%. Auto

reeled under pressure tracking the raise in steel prices while

Cummins, Exide industries, Tata Motors and M&M were down by

The domestic markets are expected to open on a sideways note on

account of yesterday’s close and the flat cues coming in from the

With the news of LIC proposing to invest Rs 1,00,000 Crs in the

Exchange Advances Declines Unchanged

current financial year (Of which it has already invested close to Rs

40,000 Crs), the market sentiment is expected to improve.

Sugar stocks are expected to witness buying interest, with the gov-

ernment deciding to raise price, quota of levy sugar in UP and

Maharashtra for the new sugar season starting next month.

FII F&O Open Interest (OI) (Rs. in Cr)

03/09/2009 %Var FII net buying

The rise in global metal prices is also expected to generate interest

For the Nifty 4,626 and 4,650 are the immediate resistance levels,

while 4,553 and 4,500 are the immediate support levels. Contracts 03/09/2009 02/09/2009

While 15,500 and 15,600 are the immediate resistance levels for

the Sensex, 15,257 and 15,100 are the immediate support levels. www.zenmoney.com Trade Statistics - (Turnover Rs. in Cr.) 03/09/2009 02/09/2009 World Indices: Nikkei benchmark index closed in the negative zone on the

back of yen’s strength against the dollar and on the outcome of the US jobless

claim, which came in worse than expected. In the export sector Honda Motors

Co, Toyota Motor Corp and Canon Inc lost 2.8%, 1.8% and 1.4% respectively.

By the close of the trading session, Nikkei was down 0.64% to close at

10214.64. In the European markets, the British benchmark indices continued

its losing streak for the fourth day as a fall in energy and pharma space

weighed on the market. Worse than expected jobless benefit claim in the US

Forex, Commodities & Major World Indices

applied pressure, while better than expected sales data from US retailers

gave support to the market at the lower levels. By the end of session, the

Particulars 03/09/2009 Gain+/loss-

FTSE was down 0.43% to 4796.75, while the CAC and the DAX were down

by 0.55% and 0.35% respectively. In the US market the indices were up on

the back of better than expected retail sales data, while some of the investors

were seen cautious ahead of the jobs data. Retail and financial space were

the top performers for the day. With the rise in metal and gold prices, rally

was witnessed in the commodity space. By the close of session, the Dow was

up 0.69%, while the S&P 500 and the NASDAQ closed higher by 0.85% and

Brent Crude Oil ($/BRL): Crude oil prices closed marginally lower on the Institutional Activity

outcome of a mixed set of economic data, where the jobless benefit claim

came in higher than expected, while the retail sales showed an improvement.

The Dated Brent Spot closed at $66.80/barrel, against the previous close of

Most Actively Traded Stocks Gold: Gold prices rose sharply as concern over economic recovery, along Total Qty Value (Lakhs)

with worse than expected economic data coming in from the US weakened

the sentiment in the equity markets. The spot gold closed at $994.40/Oz,

against the previous close of $978.70/Oz. Forex Markets: Rupee rose on the expectation of a rise in the domestic stock

market, while the demand of dollar from the oil companies and the eventual

selloff in the domestic markets towards the close of the day capped the upside

for the rupee. Rupee closed at Rs 48.93/$, against the previous close of Rs

ADRs/GDRs as on 03/09/09 Bond Markets: Bond prices closed lower as investors were seen covering

their position, while a less than announced buy back from the RBI in the

open market operation added to the weak market sentiment. The 7.02% 7-

year government securities closed at Rs 97.73 (7.38% YTM), against the

previous close of Rs 98.10 (7.37% YTM). The inter-bank call rates closed at

Inflation rose marginally to -0.21%, against -0.95% in the previous week due

Auto component maker, Shriram Pistons & Rings, is planning to invest Rs

225 crore for setting up a new manufacturing facility at Pathredi, Rajasthan,

Most Active Contracts (Value in Rs Lakhs) Symbol Instrument StrikePrice Contracts Ranbaxy Laboratories have entered an agreement with the US-based Validus

Pharma for marketing and distribution for its low cost versions of its cal-

DLF Ltd has allotted 21,690 Equity Shares of Rs. 2/- arising out of exercise

of stock options by the eligible employees under the Employees Stock Op-

Moser Baer India bagged a project to develop one mega watt solar project

from Maharashtra government in Chandrapur. Disclaimer

This document was prepared by Zen Securities Ltd (ZSL), on the basis of publicly available information, internally developed data and other sources believed to be reliable. The material contained herein is for information only and underno circumstances should be deemed as an offer to sell or a solicitation to buy any security. ZSL or its employees, may, from time to time have positions in the stocks mentioned in this document. While all care has been taken to ensure thatthe facts are accurate and the opinions are reasonable, ZSL shall not be liable for any loss or damage howsoever arising as a result of any person acting or refraining from acting in reliance on any information contained therein. www.zenmoney.com

Pakkausseloste: Tietoa potilaalle Tamofen 10 mg ja 20 mg tabletit Lue tämä pakkausseloste huolellisesti ennen kuin aloitat lääkkeen käyttämisen, sillä sisältää sinulle tärkeitä tietoja. - Säilytä tämä pakkausseloste. Voit tarvita sitä myöhemmin. Jos sinulla on kysyttävää, käänny lääkärin tai apteekkihenkilökunnan puoleen. Tämä lääke on määrätty v

Zen Daily Market Report - 04/09/2009

Zen Daily Market Report - 04/09/2009 Trade Statistics - (Turnover Rs. in Cr.)

Trade Statistics - (Turnover Rs. in Cr.)